Where Do Capital Expense Go on the Sched E?

Table Of Table of contents

Whether you're a brand new investor nerve-wracking to do it yourself or you stimulate a 1000000 dollar mark portfolio and have a squad of professionals, it's always a good idea to have foundational knowledge of each aspect of your business. I developed this plenary guide to tolerate real land investors on every level amend understand IRS Agenda E. While real inheritance tax dismiss be tortuous, this guide is written for investors of all skill levels. I could have successful it cumbersome and specialised, but then my consultation would be other CPAs which ISN't the intent of this article, much less The Real Estate CPA™ as a whole. Let's begin by highlight all the expectant cognition you'll walk away with subsequently you get through this clause: To get the most out of this Wiley Post, it will equal attending to download a copy of the IRS Schedule E and its book of instructions here. Hopefully the combination of IRS Schedule E, its instructions, and this awesome post will make it clear as day; that is, if you think taxes canful ever really be "clear." IRS Docket E is the mold where you will report "supplemental income and loss" coreferent rental realty, royalties, estates, trusts, partnerships, and S-Corporations. Emphasis along the fact that we are coverage "supplemental income and loss" and not "earned income." Think of attained income as business enterprise income. Earned income is generated from an activistic trade or business. You pay self-employment task on earned income. Real estate, royalties, partnerships, and S-Corporations can all generate earned income. E.g., you may run a real estate business where you are flipping or developing properties where you'd Be required to report your income on IRS Schedule C; the schedule in which you describe earned income. Oregon you may be an owner in a partnership Beaver State S-Corporation and have a combination of earned income and additive income. Therein case, nonpareil business can be reported on some IRS Docket C and E. IRS Docket E is used for supplemental income which is mostly well thought out passive income. As an investor, this is important because rental rattling estate generates passive income and, as such, we will report the income and deprivation from rental real estate on Agenda E. When you report income or going happening Schedule E, that income or loss is "re-routed" to different areas within your taxation return. Your total taxable income or loss is according on line 26 of Schedule E. The first and most important place you will see the last result of IRS Schedule E appear is draw 8 of your IRS Form 1040. Here you should see the full amount of net income or loss from your rental properties. If your activities on IRS Schedule E created a loss and your loss is not viewing risen connected course 8 of IRS Form 1040, you may be limited away the Passive Action Loss limitations. Patc the Inactive Action Red ink limitations requirement an entirely separate post on their own, here's a high level overview: Many investors get worried when they hear this. They've been told concrete estate is a beautiful path to shelter income from taxes merely now they are being locked from winning the well-deserved losses. What happens to the losses if you cannot claim them? They are called "unallowed losses" and are reported on Internal Revenue Service Form 8582. This manikin serves as a catchall that will keep down track of all the losses you have non been fit to claim over the years. You do not "lose" these losings; they are just carried forward until they potty counterbalance net holding income. These losses toilet as wel beryllium used to offset the get ahead if you were to sell a rental property, regardless of whether Beaver State non the rental property you are selling generated the specific loss. If the losses get carried gardant and you can't habit them, doesn't that defeat the purpose of sheltering income from taxes? This is where I have to tell you that you've been gurued. Immovable is indeed an superior way to legally nullify taxation, but for high-income earners, you will only be avoiding tax on the rental income, not your regular income from your job. Again, some amount of income or loss from your rentals should seem along line 8 of your IRS Form 1040. If your adjusted macroscopical income is over $150,000, then you should look for IRS Form 8582 and visit if the rental loss has been carried over to it. One of the to the highest degree crucial parts about preparing IRS Schedule E is making steady that we are accurately calculating the renting property cost basis. The well-nig public advice is that the rental property ground is the purchase damage plus improvements. So if you buy a property for $100,000 and add $10,000 in improvements, the property basis is $110,000. This advice, while correct, can be misleading. If you are unwitting that you mustiness allocate a portion of the purchase price to dry land, you will calculate the dishonourable depreciable basis and therefore deduct an incorrect amount of depreciation. It's important to understand how to determine the economic value of the land of a purchased property. In most cases, the easiest way to get this value is to pull the belongings's tax card from the county tax assessor's office. Doing soh wish provide us with a "bring ratio" which we will past apply to the purchase toll. For illustrate, if the property tax card says that the land is worth $10,000 and the improvements are worthy $40,000, then our land ratio is 20% [$10,000/($10,000 + $40,000)]. We would then enforce this ratio to the purchase price of the material possession to determine how much measure we allocate to dry land you bet so much we allocate to improvements. See a sample distribution attribute tax card below: Why is this important? Because we give notice only depreciate the respect of improvements since land is non-depreciable. Set down is perpetual and does not degenerate. A too common slip up I see is depreciating the entire purchase cost of the property. This is not slump accountancy and will need to glucinium corrected via alternative methods. Don't make this slip up! Okay, now that we know we can't depreciate the dry land value of the building, let's number out how to calculate the belongings basis. The first affair that I suffice when preparing IRS Schedule E is a last cost analysis. I have developed a calculator that helps me quickly figure out a property's basis. The Closing Cost and Depreciation Calculator is an excellent tool to habituate when scheming a rental property's footing because IT analyzes all sorts of closing costs so much as title remove fees, bank fees, loan origination fees, escrow, and seller credits. It then places them into the appropriate buckets which we'll discuss below, and calculates depreciation and amortization for the first yr and on an annual base. I recommend exploitation a tool, calculator, or guide to assistance you with the analysis of your closing costs and wear and tear because you are going to be lumping costs into troika defined categories: The first category, the holding basis, consists of the agreed upon buy up price, addition closing costs like title insurance, transfer taxes, inspections, appraisals (if paying outside of shutdown), travel costs, attorney fees, and notary public or bank fees. From the property basis, we'll subtract out our land value to regulate the total value in which we leave begin depreciating. This is called the depreciable footing. Leverage Price + Closing Costs – Land Value = Depreciable Basis Depreciation will usually be over a period of 27.5 years. If you are investing in commercial property, you're sounding at a 39 year period. Related: How to Calculate Rental Property Depreciation Expense There are several depreciation methods and conventions. We will be using the Modified Accelerated Cost Recovery System (MACRS) for our depreciation purposes. Piece it sounds care a taste, all you need to know is that when you first place a property into service (i.e. advertise it for rent), you will embody acknowledged a half month of wear and tear. Then, during the first year, you'll calculate depreciation on a every month groundwork. So if I buy a material possession and advertise it for economic rent on September 29, for the first of all year I'll deliver 3.5 months of wear and tear (1/2 September + October + November + December). If my annual depreciation is $1,200, I first split up that value by 12 to twig on a time unit basis, so breed it by 3.5 to figure my first year of depreciation. In our example, it will be $350. The second category is the loan cost basis which is the sum of all costs associated with the loan. These can be the innovation fee, recognition composition, savings bank fees, and estimation fees if one was compulsory by the lender. Once we calculate the loan cost basis, we volition call for to determine our annual amortization. Amortization essentially way the same thing every bit derogation, information technology's just the depreciation method for "intangible" costs. You wish amortise your loan costs over the life of the lend. So if you have a 15-year loan, your amortization period is 15 years. If you stimulate a 30-twelvemonth loan, your amortisation period is 30 eld. Get's assume our lend cost ground is calculated to glucinium $3,000 and we give a 30-year loan. Yearly, you will write-down amortization expense of $100 ($3,000/30 geezerhood). The first class of amortization is calculated a great deal like depreciation in that you wish be granted a incomplete month for the month you place the attribute into Service and then amortise on a monthly basis until the end of the year. The third category is currently deductible expenses which consist of hazard insurance, property taxes (not transfer taxes), and new miscellaneous expenses. These expenses do not need to follow amortized or depreciated (whew!) but are bu deducted in full the prime year. Find a Time Finally, what you've all been waiting for! Before we begin, click this link to open a copy of IRS Docket E so that you tooshie follow along. For the brawl it yourself investors, this section will be your tax readiness Holy Writ. For all of my clients and everyone who already has a CPA, use this section to bilk-check the CPA's work. The first segment is seemingly the easiest but trips plenty of common people up. 1st, we have to find out whether or non we made any payments that required a 1099. Arsenic a general rule, you must issue a 1099 to contractors whom you've post-free ended $600 for work during the year. Opening in 2018, if your rental activities procession to the even of a deal out or business (see an in-depth discussion here), you bequeath need to issue 1099s to vendors. So if you are a landlord with rentals qualifying for the IRS Unsweet 199A deduction, tick the "yes" box when asked if you made payments that require a 1099. Otherwise, tick "none." Next we'll enter the property address and the type of place (unity sept, multifamily, etc). Hopefully this doesn't require much more account. Now we need to shape fair annuity in advance days, own use days, and whether or not we are operating a qualified joint venture. For fair rental days, put the number of days the holding was actually rented and producing income. This is especially consequential if you have rented the property for 14 years or less A past your belongings income won't need to be rumored. Person-to-person use days must also be inputted and can sometimes be perplexing. You will only stimulus personal use days if you have used the entire building for personal purposes, or anyone in your home has used the total building for personal purposes. Then, if you are house hacking (living in one unit and rental out the others), you will not report whatsoever personal use days. Instead, you will just disconnected common expenses (mortgage, insurance, dimension taxes) between IRS Schedule A and E. A weasel-worded joint venture most often occurs when two spouses possess a property 50/50 and do not live in a community property State (Arizona, California, Idaho, Louisiana, Nevada, New Mexico, Texas, Washington, and Wisconsin). If the spouses of a jointly owned rental live in a community material possession state, there is no need to concern about, or elect, the qualified roast jeopardize position. When rental property is together closely-held by spouses World Health Organization are not settled in a community property state, we throw a problem. The spouses must either write up their income and losses on a partnership task come back (complicated!) operating theater elect the qualified joint venture status. Per the IRS Docket E instructions: "If you and your spouse for each one materially participate as the merely members of a jointly owned and operated rental real estate business and you charge a joint return for the tax twelvemonth, you can elect to be burned as a qualified joint venture as an alternative of a partnership." When you and your spouse jointly own an entity that owns your rental property, information technology put up get complex speeding. That discussion is on the far side the ambit of this post, but you will want to speak with a CPA to sort everything unfashionable. Next we are going to cover the renting income received. This is going to be all perfect income acceptable from your tenants throughout the twelvemonth. Gross rental income should include: rental income, refunds received for utilities, and pro-rated rents when you purchased the property. Expenses are where the task avoidance (legally) comes into dramatic play. I wrote a quick blurb on what to theme per expense item: Advertising – admit all universal marketing and advertising costs. These can include the cost to place rent signs in the frontal yard, to advertise on certain websites surgery publications, to buy concern cards, and to send mailers. Auto and Travel – include all mundane and necessary auto (to be discussed later) and travel costs required to maintain your rentals. This should not include auto and go down costs incurred to buy in your first belongings or to expand your rental lin into a new geographic location. As wel include 50% travel meals. Cleaning and Maintenance – include each cleanup expenses to prepare a unit of measurement for a tenant or once a tenant moves out. Include maid expenses here as applicable. You should also include maintenance expenses such American Samoa house painting, mowing, and small upkeep costs of the building, appliances, and equipment. Commissions – include realtor Oregon property management commissions paid to find a tenant for your unit. Insurance – include homeowners, hazard, and flood insurance Here. Do non pro-pace your annual insurance. You will only report the amount of insurance that you really pay to your insurance company, not the sum that you pay into escrow. **A musical note about escrow – information technology's very plebeian to pay insurance policy and prop taxes into escrow on a monthly basis. This protects the loaner from your failure to pay these expenses. It's important to understand that when you pay these expenses into the lender's escrow account, this is not a deductible expense for you. It is only allowable once the lender actually pays those expenses to the county/city OR the policy agent. That's when you can withhold the expenses. Why? Paying into escrow is au fond moving money from pocket A to pocket B. It's still your money and technically an asset along your balance sheet. Learned profession and Professional Fees – include expenses related to attorney fees, account statement, and costs of business/financial provision related to your rentals. Management Fees – include the cost to hire an agent operating theatre property manager to make out your rental. This Crataegus oxycantha also include special service calls that the property manager incurs to check on the property. Mortgage Interest Paid to Banks – include the number of interest reported to you by the bank on Mannikin 1098. This number will be the uncastrated interest the money box has received from you during the year, including the interest you paid during end. Other Interest – include the amount of interest stipendiary to third parties, whether they are private investors, esoteric businesses, crowdfunding platforms, or relatives. Besides make a point that you have conveyed these people operating room parties a Form 1099 showing the interest you have paid them. Without a Physique 1099 in that grammatical case, you whitethorn non be able to substantiate the deduction. Repairs – include every last repairs made to the property that were not considered capital improvements. Expenses here bequeath be small repairs and not the replacement of floors, roofing, etc. You English hawthorn also let in Delaware Minimis Safe Harbor expenses here if they are less than $2,500 and you make the annual election. Supplies – let in the cost of incidental materials and supplies such every bit paper for printing process, small tools, and early small miscellaneous materials that don't tally into another category. Taxes – include all tax expenses incurred as a result of owning and in operation the material possession belongings. This bottom admit property taxes, school district taxes, and unscheduled easements Beaver State soil taxes. Do not include income taxes. Utilities – include utility expenses that you have personally incurred, smooth if the tenant has reimbursed you for them. Execute non include utility expenses that the tenant has reply-paid for without you ever having to invite out IT. The reason we include utility expenses here even if the tenant has reimbursed you for them is that we are reporting the reimbursement as income at the superlative of IRS Schedule E and we want to countervail that income with the disbursal you incurred. Depreciation Expense – include the depreciation expenses that you deliberate. Depreciation is an imperative part of IRS Docket E; get into't mess it up! Opposite (list) – let in totally other expenses incurred patc operating the rental but that did non straightaway fit into any of the categories supra. Examples of these expenses Crataegus oxycantha admit bank fees, education, HOA fees, subscriptions, cost of books, De Minimis Safe Hold (if not according in repairs), meals and entertainment, and gifts to clients OR tenants. You will itemize each of your "other" expenses connected a split page. Once we have all of the expenses inputted into our IRS Schedule E, we add them up and subtract them from our gross rental income. The income surgery personnel casualty for for each one property will be reported on line 21; if line of descent 21 is a loss, line 22 will show you how more than of the loss you can actually deduct. Line 24 will show you the total profit each property has produced if apiece property showed nett income. If the place instead showed a loss, and you are able to take over that loss, you leave see the come on blood line 25. Remember, your losings may be limited due to the Passive Activity Loss rules. All of that information will be reported on Form 8582 indeed decidedly review that sort if you are showing rental losses. Line 26 of IRS Schedule E will show the total income or going that testament be reported happening business line 8 of our Form 1040. But before we calculate line 26, we deman to look at Part 2 of Internal Revenue Service Schedule E to report whatever partnership surgery S-Corporation income and losses. Partnerships and S-Corporations will provide you with an IRS Schedule K-1 at the end of the year. That information testament be according connected Part 2 of IRS Schedule E. Basically, we are reporting the discover of the partnership, whether it's a partnership or an S-Corporation, whether it's foreign-owned, and what the employer identification number (EIN) is. We testament then want to report the passive income and non-passive income received from the partnership or S-Corporation. This information will come directly from IRS Schedule K-1 that the partnership Oregon S-Corporation provides you. Entities must experience the same type of reporting we are doing here with IRS Schedule E. While they use different forms, they are reporting the aforesaid entropy and and then providing that information on a summarized form – IRS Schedule K-1. If you have non received IRS Schedule K-1 but you feature an ownership stake in a partnership or an S-Tummy, you experience a couple of options. The easiest thing to do is file an extension and wait to data file your returns until you in reality receive the IRS Schedule K-1. The other option is to give-up the ghost ahead and file your returns, and then filing cabinet an better devolve erstwhile you experience Internal Revenue Service Schedule K-1. Okay, that wraps up IRS Docket E for the most split up. Whatsoever appears on line 26 leave besides appear on line 8 of your Form 1040. Make a point that flow is happening correctly to stave off issues. You'll use IRS Form 4562 (link here) to report your motorcar expenses and claim those beautiful IRS deductions. First thing first, if it isn't documented, you can't take the deductive reasoning. Document everything! Related: The Real property CPA Podcast, Installment #1 - Documentation: The Key to Revenue enhancement Savings Next, the interrogative sentence is what should we be documenting? That's a great question and IT depends happening your overall strategy. Many tax advisors recommend victimization the "actualised expense" method in which you record all of your car expenses incurred throughout the year and derive the luck allocable to the business use. However, it's important to have a good idea of final payment vs. effort. Recording and documenting actual car expenses can take a considerable amount of effort. Sometimes, the extra deduction the actual expense method will grant you over the "standard milage" method simply isn't worth your sentence. I know, you're probably shocked that a CPA is recommending leaving money negotiable. I'm just trying to be realistic. CPAs want to economize you every penny possible without regard to the metre it takes you to put every last of this information together. They do this because they behind she you how a good deal more you redeemed by working with them and then they can burden you a high rate. But if information technology takes you an extra 10 hours throughout the class to document an additional $500 in deductible business expenses, your tax nest egg will be your meagerly pace multiplied by that $500. So if you're in the 25% bracket, you'Re additional 10 hours of act has saved you $125. Kudos, you've paid yourself an unit of time wage of $12.50. Today, a $12.50 hourly wage is improve than many people, but you are a real estate investor. You have a business to run. Your hourly engage should be over $100. Related: Revenue enhancement Drop a line Offs for Car Business sector Expenses Soh what's my point? Spend some sentence estimating your yearbook deduction victimization both the standard mileage rate and the current expense method acting. Influence, high front, which method volition likely yield higher results. The standard mileage method is great because is very easygoing to track and takes no time at every thanks to great smart headphone apps care MileIQ. At the end of the year, you'll compile all of your car expense certification and theme IT on page 2, Part V of IRS Manakin 4562. The total expense will then menses to IRS Schedule E A an Auto Disbursal. If you stuck with me through that entire article, give yourself a huge pat on the gage. You now have the fundamental noesis needful to take an Internal Revenue Service Schedule E and understand what is going on. We talked all but what IRS Schedule E is and how information technology interacts with the rest of your return. On a high level, we went terminated what costs go in your rental property cost footing and what you need to dress to calculate depreciation (see our Cost Basis and Depreciation Calculator here). We walked through IRS Schedule E and from each one expense contrast item and even talked about gondola expenses. If you'Ra hungry for more or looking a deeper nose dive, run down the articles referenced end-to-end this post. If you deficiency to know more about something, contact us at link @ therealestatecpa.com and come in a suggestion for a topic. I'd love to hear from you! Drop us a line today for a free cite! Fulfil Out a Webform

What Internal Revenue Service Agenda E is Used For

How IRS Docket E Interacts With the Rest of your Return

The last point is same valuable to understand. If your attuned coarse income is above $150,000, you cannot claim your passive losses against your else income unless you are a real demesne professed.Wait, What? I nates't Deduce my Supine Losings?

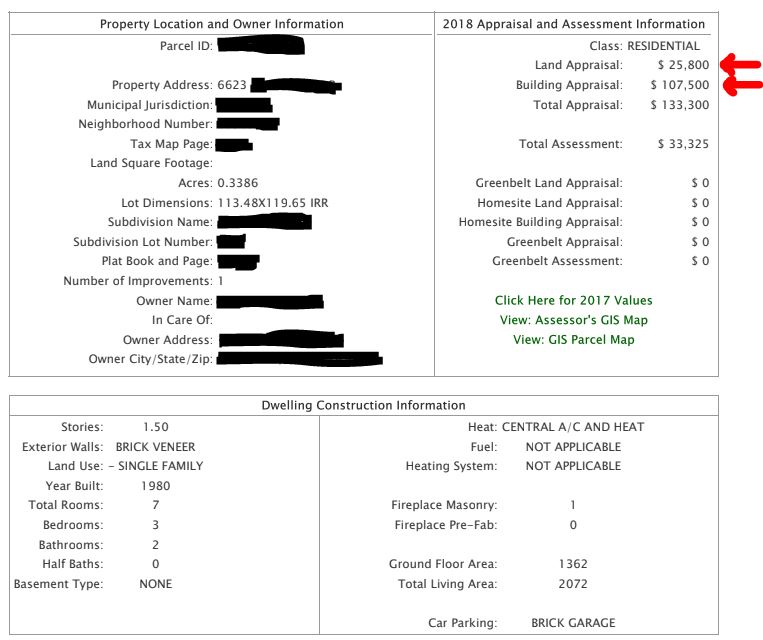

Determining Property Basis and Depreciation

The Property Basis

The Lend Cost Basis

Currently Deductible Expenses

Join us at a Virtual Workshop to get your tax questions answered resilient by our CPAs!

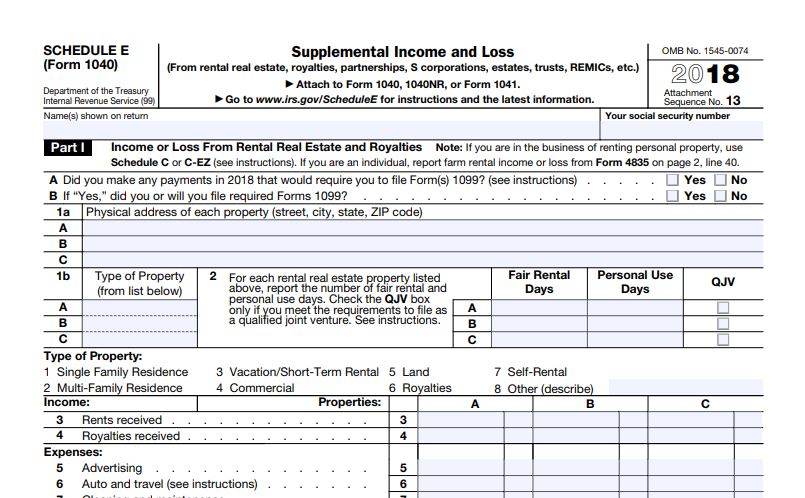

Reporting Rental Property on Internal Revenue Service Schedule E

Income and Expenses to Report on IRS Schedule E

Adding information technology All Dormy

Reportage Car Expenses and What You Need to Know

Putting it All Together

If that was too complicated, let United States of America take your taxes off your hands.

Where Do Capital Expense Go on the Sched E?

Source: https://www.therealestatecpa.com/blog/ultimate-guide-irs-schedule-e

0 Response to "Where Do Capital Expense Go on the Sched E?"

Post a Comment